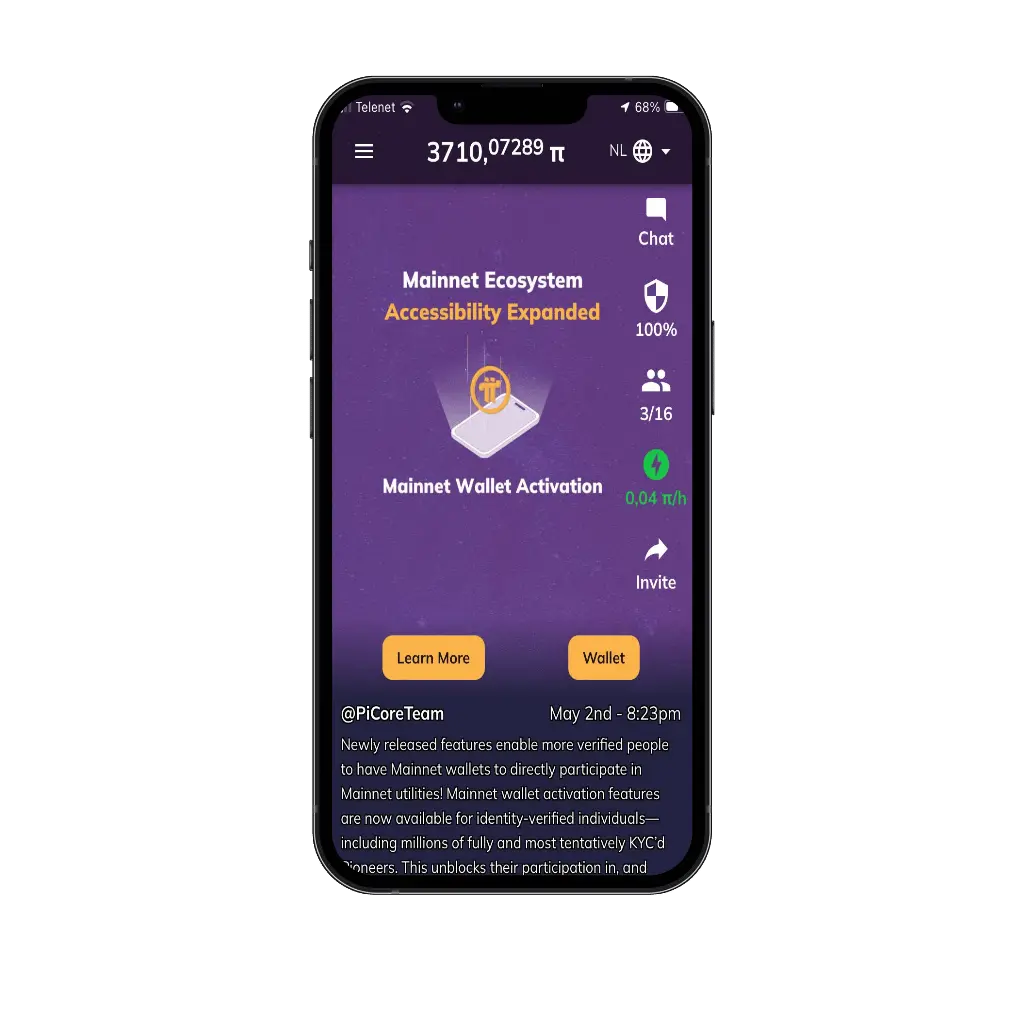

Pi Network: Mine Pi with Your Mobile Phone

Join millions earning Pi cryptocurrency with just a daily tap. No battery drain, no costly equipment — simple, eco-friendly mobile mining for everyone.

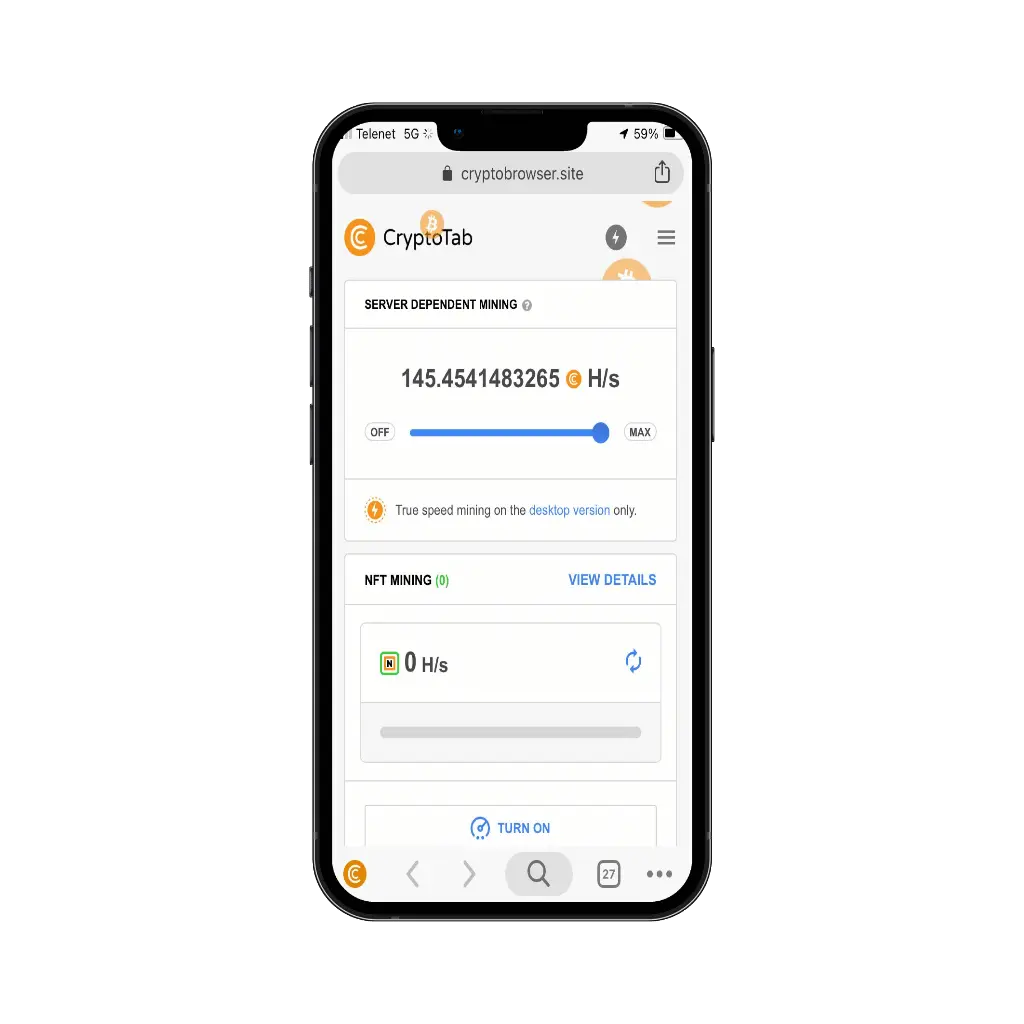

CryptoTab: Earn Bitcoin While You Browse

CryptoTab lets you mine Bitcoin effortlessly as you surf the web. Lightweight, fast, and easy to use — start earning crypto today just by browsing!

Bee Network: Earn Free Crypto on Your Phone

Join Bee Network to earn Bee cryptocurrency for free through mobile mining and social referrals. Start building your crypto rewards easily today.

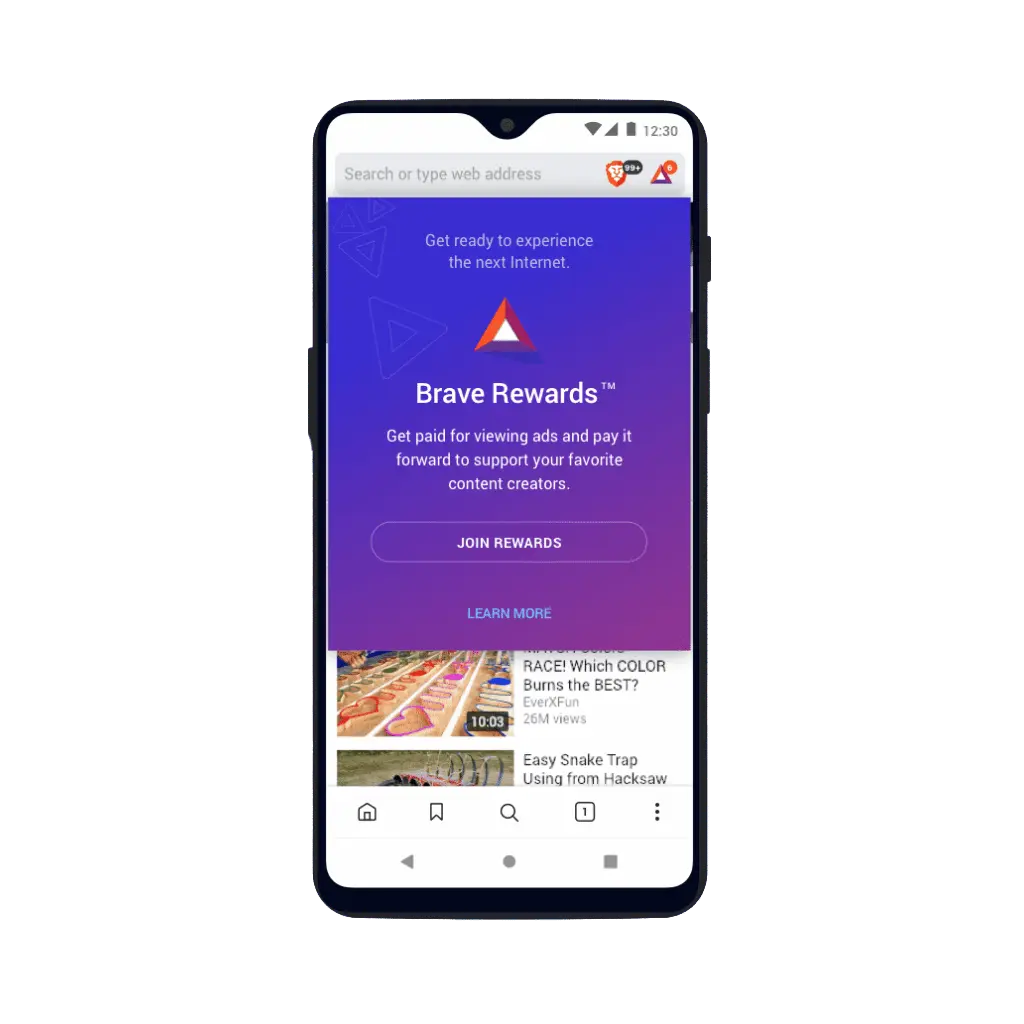

Brave Browser: Browsing with Crypto Rewards

Use Brave Browser to enjoy faster, ad-free browsing while earning Basic Attention Token (BAT) for viewing privacy-respecting ads.